2026

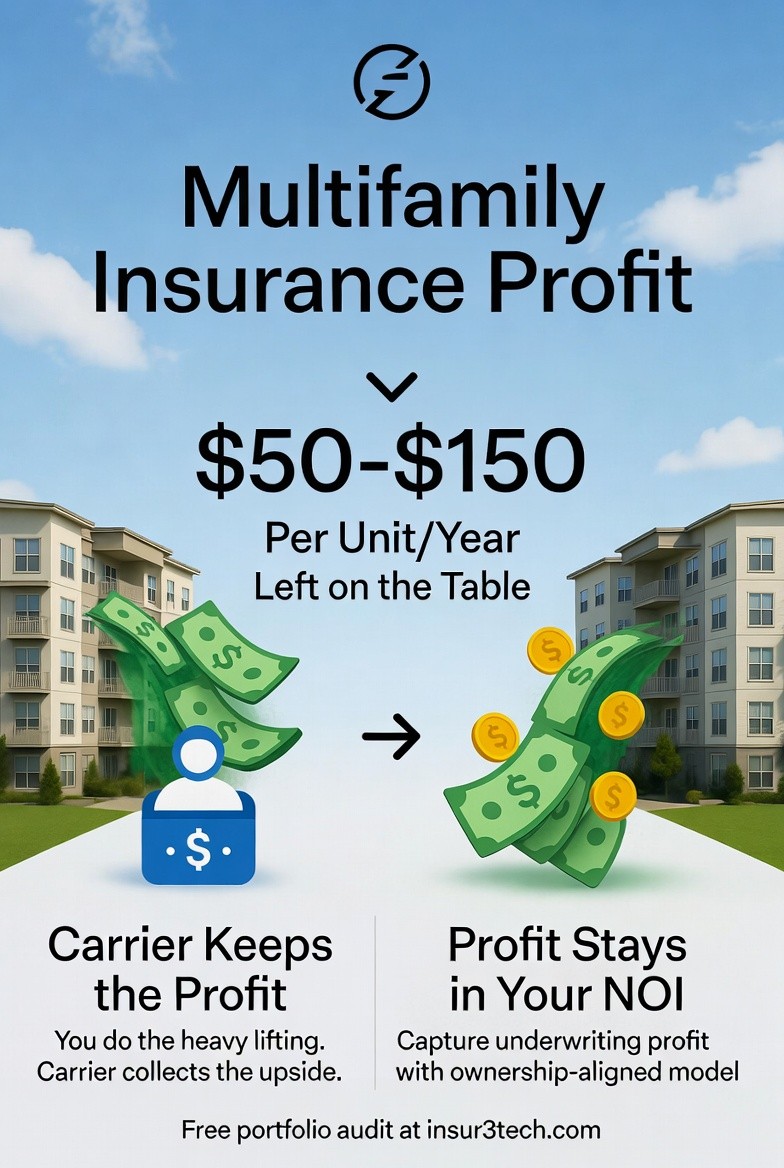

After talking to hundreds of regional managers and on-site staff, I’ve seen the same pattern over and over: properties keep quietly handing third-party carriers $50–$150 per unit per year in pure underwriting profit. And for work the operators and their teams are already doing themselves.

Everyone realizes it’s happening, but no one knows they are getting the short end of the stick.

The Real Job of On-Site Teams (And Who Actually Profits From It)

Ask any property manager or regional what their day-to-day looks like and you’ll hear the same answer:

Managing residents

Preventing maintenance issues before they escalate

Performing move-out inspections

Being the first point of contact when something goes wrong

Tracking certificates of insurance (COIs)

Chasing renewals

Coordinating and turning damaged units

In other words: they’re doing risk management and loss prevention every single day.

Then I ask the follow-up question: “When you do that job really well and everything goes according to plan, who benefits the most financially?”

There’s usually a long pause.

Then the answer: “The insurance company we're sending residents to.”

That’s the backwards part no one talks about.

How the Current Structure Actually Works (And Why It’s Broken)

You do the heavy lifting.

Your team prevents claims, enforces compliance, and handles all the admin work.The carrier collects the upside.

When claims stay low (because your property is well-run), the carrier keeps the underwriting profit. Your NOI doesn’t move. You get the same admin fee whether you have 5 claims or 50.There’s no line item for the profit you’re subsidizing.

No one sees “Underwriting profit given to Assurant this year: $127,000.” That money just disappears.

On paper it feels fine, you’re getting your small admin fee! In reality, you’re carrying the full operational burden and risk while a third-party carrier (who has never walked your property) walks away with the real money.

The Math Most Operators Never Run

For most portfolios, the hidden underwriting profit sitting on the table is $50–$150 per unit per year.

That’s not a rounding error.

On a 500-unit community, that’s $50,000–$75,000 in annual profit currently flowing to a carrier instead of your bottom line.

On a 2,000-unit portfolio? $200,000–$300,000 every year, money that could be showing up as retained earnings or distributed back to owners.

Yet most operators are still hunting for nickels in the couch cushions with rent optimization strategies while the insurance carrier quietly walks out the front door with the TV.

Why the Existing Model No Longer Makes Sense

The only logical way the traditional resident insurance structure would make sense is if the carrier sent people to:

Walk your properties

Enroll residents

Track COIs

Handle claims

Turn damaged units

Except they don’t.

Your team does all of that. The carrier just cashes the checks you send them every month.

The Better Way: Capture the Profit Instead of Sending It Away

The fix isn’t complicated — it’s structural.

Run the actual numbers on what underwriting profit looks like for your portfolio. Then shift to a profit-sharing, ownership-based insurance model where the economics stay inside your ownership group instead of leaving the building.

Platforms like Insur3Tech.com were built exactly for this: they let operators participate directly in the underwriting profit on the resident liability and related insurance programs their residents are already paying for.

Same coverage. Better claims process. Upside profit belongs to you.

But now the profit shows up in your NOI instead of a carrier’s balance sheet.

How to Stop Leaving Money on the Table

If you’re a multifamily owner, operator, or regional manager tired of subsidizing third-party insurance profits, the first step is simple: know your number.

Most operators have no idea how much they’re actually leaving on the table until they see the math.

Want to see what $50–$150 per unit per year looks like on your specific portfolio? I offer free 20-minute portfolio audits that show exactly where your current resident insurance structure is leaking profit, and how much you could be capturing instead.

Just fill out an NOI Estimate or book a quick call. We’ll run the numbers on your portfolio and show you the difference in black and white.

The structure has been backwards for years.

The good news? It doesn’t have to stay that way.